Bob Murphy has a post, which starts with a parody:

Suppose someone asks you, “What was the stance of US monetary policy in mid-1980? Pretend you are a Market Monetarist answering.”

BOB TRYING TO PASS AS A MARKET MONETARIST:

First thing, we would not look at interest rates; that is a totally misleading indicator. As Sumner tells us in this post, “Interest rates tell us nothing about the stance of monetary policy.” In context, he is saying that the Fed interest rate cuts in the early 1930s were still consistent with very tight policy.

Instead, let’s look at NGDP and unemployment: (and puts up a version of this chart)

And says:

Oh man, there’s a smoking gun, right? The unemployment rate skyrockets in the middle of 1980, while NGDP growth (blue line) collapses. (The blue line is the level of NGDP, so you can see that it falls way below the previous trend starting in 1980.) Think of all the employers who had signed wage contracts during the late 1970s, and all the consumers who took out home mortgages, expecting NGDP to grow at a brisk pace. The rug was pulled out from them by the tight-fisted Volcker, right around mid-1980.

I said parody, because to a market monetarist it would be: “Let´s look at NGDP growth and inflation”.

Changing the chart above to accommodate (beginning the chart in mid-1979 to coincide with Volcker becoming Fed Chairman and extending to mid-1985 that more or less defines for Volcker “mission accomplished):

We gather that monetary policy (NGDP growth) was being tightened as the US went into the 1980 recession (Jan-Jul 1980). However inflation was still rising so, in a sense, monetary policy was not “tight enough”.

Coinciding with the end of the 1980 recession monetary policy becomes “expansionary”. NGDP growth rises and inflation still increases for a while. In mid-1981, monetary policy tightens significantly, with both NGDP growth and inflation coming down. At the end of the 1981-82 recession, NGDP growth increases and inflation continues to decline, indicating monetary policy is neither “tight” nor “loose”, but “just right” to stabilize the economy.

Most people knew, when Volcker came along, that it wouldn´t be easy to conquer inflation. Over the previous 15 years of high, rising and volatile inflation, inflation expectations had become entrenched. Moreover, since the early 1960s, it was the rate of unemployment that “governed” monetary policy. Also, as clearly stated by Arthur Burns during his tenure as Fed Chairman from 1970 to 1978, inflation was not a monetary phenomenon, being the result of, depending on the circumstances, union power, oligopolies, powerful oil producing countries.

To Burns, monetary policy could only try to mitigate the effect on unemployment of those real (or supply) shocks.

So, when Volcker´s early tightening resulted in a 2-percentage point rise in unemployment, from 5.7% to 7.7% while inflation (due to lack of credibility given the go-stop style of monetary policy over the previous 15 years) continued to rise, the Fed “backtracked”. The attack on inflation one year later proved successful, although costly in terms of unemployment. Lesson: It´s not easy to break inflation expectations!

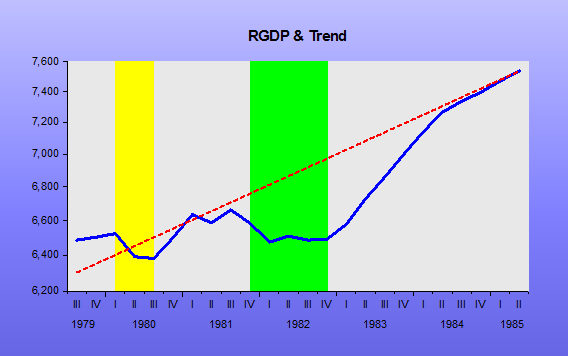

As the next chart shows, the cost was high, but temporary, because the economy regained its previous real output trend level path.

From then, until the end of Greenspan´s tenure, the economy experienced a “Great Moderation”. With the mistakes made by Bernanke, and continued with Yellen the economy has been downgraded to “Secular Stagnating”!

Nice and Informative…

“I said parody, because to a market monetarist it would be: “Let´s look at NGDP growth and inflation””

-Nope. Scott Sumner supports looking at NGDP levels and at unemployment. I distinctly remember Scott saying somewhere (in one of his posts between 2014 and today) that one of the ways the Fed should have known when to loosen in pre-9/15 2008, even in the absence of NGDP data (which comes out quarterly) was to look at unemployment. Of course, the CPI year-to-year inflation rate was quite high until September 2008, and Scott repeatedly claims inflation is a totally worthless measure.

pithom, “Look at NGDP growth and inflation” is actually a Bernanke, channeling Friedman, saying. I´ve argued that inflation is not so good as a guide because it can get sidetracked by real shocks. That leaves NGDP. If Scott said to look at unemployment he must have had a few drinks too many!

Bernanke is not a market monetarist. Sumner is. Sumner does not support looking at inflation. Bernanke does.

And, though I can’t find the specific post (it might have been on Econlog), I’m pretty sure he said something like that for pre-9/15 2008. What’s sauce for 2008 is sauce for 1980.

Pithom, I know BB is not a MM, but Friedman was an M! and BB was “replicating” him. IF Scott said to look at unemployment, his mistake. Because why should you look at a real variable to help gauge the stance of monetary policy? Just because RGDP growth faltered and unemployment went up (due, maybe, to a real shock) doesn´t mean monetary policy was “tight”. It could even be “easy” like during most of the 1970s, whe NGDP growth was on a rising trend!

Ah, Marcus, but NGDP growth also faltered severely for a quarter in 1980. Wouldn’t cause a recession now, would certainly have done so in the late seventies.

BTW, I’m E. Harding, in case you couldn’t tell from my Gravatar and my link to my blog in my name.

EH, I have a hard time understanding the attention given to noisy quarterly figures (annualized or not). In 80Q2 NGDP annualized growth faltered (0.5%). In 80Q3 it was up 9% and 20% in 80Q4. How does that change the story I told?

Well, I interpret that to mean quite tight money in Q2 (which, not coincidentally, occurred during soaring unemployment and faltering RGDP in Q2) and very loose money in Q4. Simple enough. The recession was over by August. It was the shortest in U.S. history, and ended, not coincidentally, when loose money returned. I don’t see any evidence the 1980 quarterly figures are “noisy”.

That´s all recounted in the story I told. So I don´t see your point.

You can look at interest rates if you want to go through a a whole bottle of Advil and at least ten research tomes before making heads or tails of it. The comparison between NGDP and inflation is the easier way to think about it.

And if Scott said something about unemployment, it likely was in regard to the context, like all of these other things are happening – a financial crisis, Libor rates going though the roof with the exchange rate of the dollar, and oh boy, unemployment is spiking – perhaps monetary policy is too tight. I don’t want to put words in his mouth, but that doesn’t seem to me like it means he thinks any of those in themselves are the ultimate way to judge the stance of MP.

E A Harding, you are getting a bit too like Jason Smith at Information Transfer Economics, seemingly determined to miss the wood for the trees. The overwhelming majority of posts at Money Illusion are clear. Finding one or two mistakes, or spotting a bit of hyperbole to provocatively make a broader point, is a game not worth the candle.